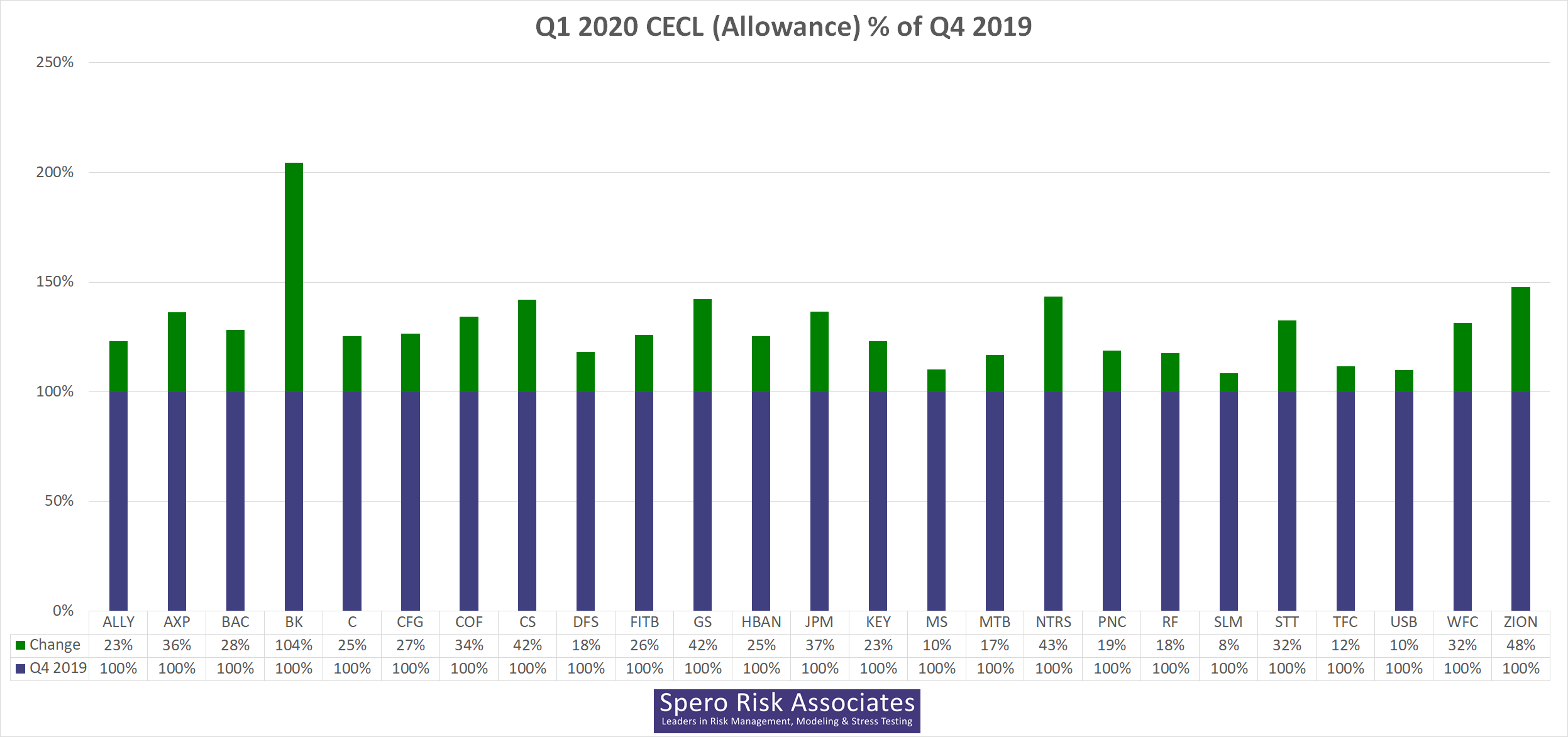

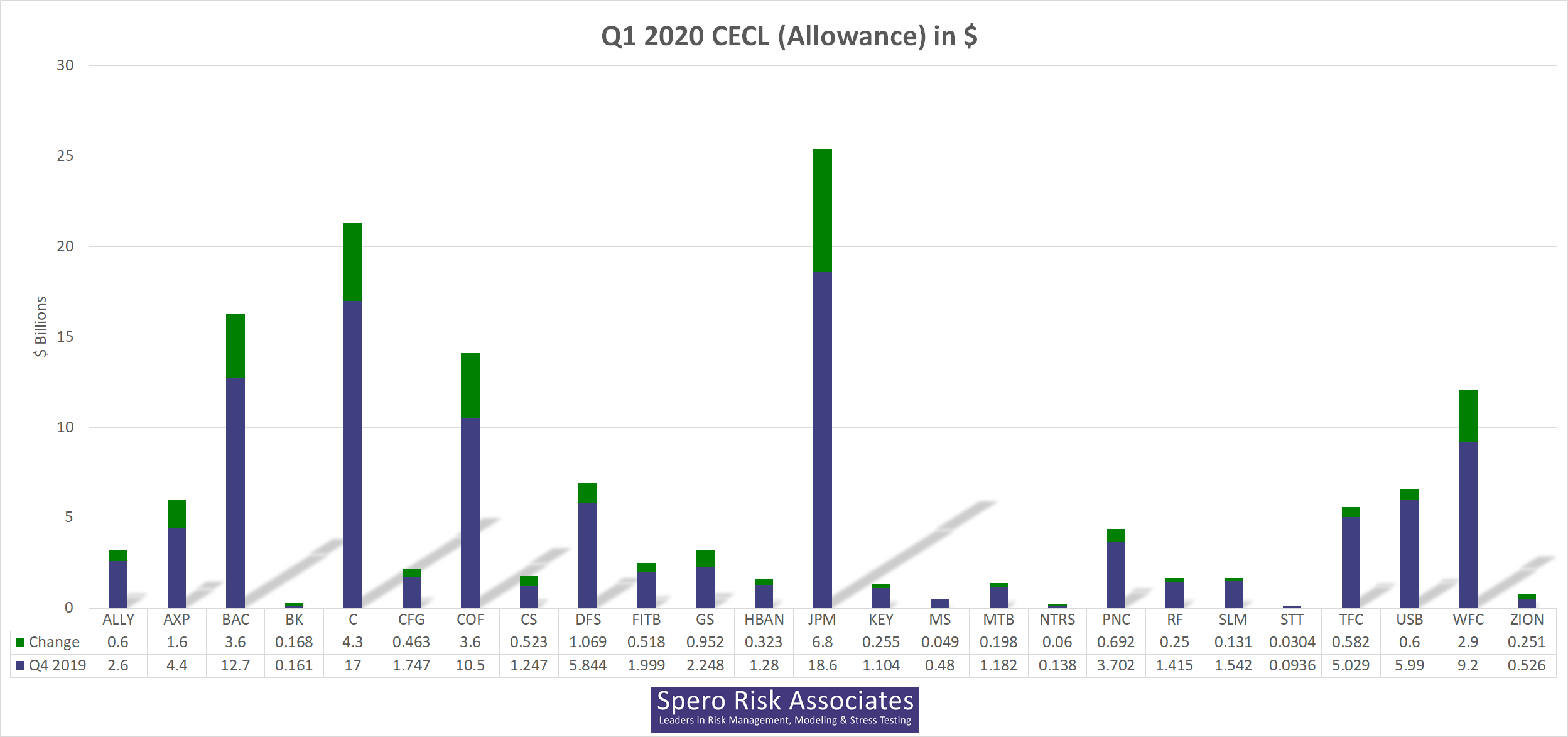

Below are two graphs that show Q1 2020 credit reserves for large, domestic (mostly CCAR) banks—for all large banks reporting earnings as of April 24, 2020. So far, no bank on our list has delayed its CECL implementation–as permitted under the CARES Act.1 Both graphs show the initial CECL reserves, i.e., as of December 31, 2019/January 1, 2020, and the quarterly change–the first in dollars and the second in percentages.

What’s missing in these graphs is a notion of how much each bank’s Q1 2020 CECL reserve differs from its Q4 2019 ALLL under the incurred loss method; we’re using the beginning of the year CECL reserve, which is already adjusted. You can get a sense of the difference from the change in methodology through banks’ initial CECL estimates. For example, Sallie Mae’s credit reserve went from $441 million—incurred loss—to $1.6 billion with CECL. Its CECL reserve rose by only 8% from the beginning of the year—as shown below—but the entire allowance has increased by about $1.15 billion, or about 261%, to approximately eight percent (8%) of loans!

When the banks release their 10Qs, we’ll try to provide numbers for specific portfolios, e.g., cards, autos, etc. Currently some banks list the allowance for each loan type, while other provide a grosser division between only consumer and commercial loans.

By the way, it might be possible to estimate a “normal” Q1 allowance by taking the ratio of the initial allowance as a percentage of total loans (at the beginning of the year) and multiplying by Q1 total loans. The difference between the the Q1 allowance and the “normal” Q1 allowance can be thought of as the Corona Virus Effect; however, we think it’s easier to think of the entire change as the Corona Virus Effect without much loss of precision. We have more to say about CECL and the Corona Virus from a modeler and executive’s perspective.

Lastly, in its first release, Morgan Stanley’s percentage change didn’t match the dollar values shown; so, the percentage change that is shown is our calculation.

- As we argue in CECL and the Corona Virus, such a delay could only be interpreted negatively. ↩