Since The Crisis, the lending environment has been relatively calm and stable.12 Some think that’s evidence of better risk management.3 Alas, periods of calm are not proof of resilience against harm, and in fact, they may obscure risks that may define the next downturn.

Better Risk Management? Six Questions to Ask

The Question: Is it really better risk management? Here are six questions to help answer that one.

- Can we be deceived by good times?

- Do unprecedented levels of value exacerbate the problem?

- Has increased supervision and risk management reduced risks?

- Is your portfolio more like a river or the sea?

- Is it really as calm as it seems?

- Are all innovations truly positive, especially for lenders?

And of course: What should a banker do with the answers to these questions?

A Regime-based Perspective

Let’s set the stage by describing credit loss behavior over the long-term. For most portfolios, credit loss rates are essentially bimodal. There are (only) good times and bad times, and by avoiding unfortunate errors, it’s hard to lose much money in good times, although you will almost always lose more on riskier borrowers than less risky ones.

Loss rates are low—until they’re not, and when they’re not, they are much higher—often an order of magnitude or two higher going from single-digit basis points to whole percentages or more. There is very little middle ground—except when crossing the long-term average on the way up or down. Because the long-time average is substantially higher than the average during good times and because the majority of times is good, bimodal regimes can be misleading.

1. Can we be deceived by good times?

Don’t be fooled by success. Recognizing that you’re in low-loss regime makes it less likely you’ll draw the wrong conclusion that “things are different this time!” simply because recent losses, even for a long, recent period, like a decade or more, have been lower than in the past.

During good times there will be recent evidence—perhaps even substantial evidence—that had looser standards been in place in the recent past, profits would have been higher. That’s because with marginally looser standards, interest revenue would have been earned, and credit losses, while higher, would likely not be high enough to offset the increased revenue.

The question is whether your expectation of future losses, based only on recent performance, is reasonable? The marginally looser standards will usually cause you to lose a little more during good times, but from our experience, they’ll cause you to lose significantly more during bad times. That’s what makes marginal borrowers marginal; they’re much more at the mercy of the broader environment and economy.

Lowering credit standards during good times starts a race: will the marginal borrowers repay before they’re negatively affected by a downturn and then can’t pay?

We note that looser standards may be masked or disguised as special programs for special borrowers, who “aren’t as risky as they seem.” Maybe they aren’t. But for a novel program, is there evidence of how those borrowers would have performed in the last downturn—even circumstantial evidence—and not just during recent good times?4

2. Do unprecedented levels of value exacerbate the problem?

For any type of portfolio—retail or wholesale, secured or unsecured—we try to include clear measures of (underlying) value in our loss forecasting models. In such models, economic variables can play one of two roles and sometimes both: (1) as indicators or proxies of a customer’s or collateral’s value, and (2) as indicators of overall market conditions.

In our work, we find that a clear indication of a portfolio’s risk—i.e., its potential for loss—is the percentage of loans put on at or near peak value. Obviously, no one knows that a peak occurs until values decline, but it is relatively easy to determine when values pass previous highs (and whether those new highs were reached gradually or quickly).

Experience shows that gradual increases tend to have smaller decreases in a downturn. If you are not convinced, go to FRED and search various city or state-level HPIs. For example, consider price changes in Pittsburgh and Las Vegas, prior, during and after The Crisis.

For certain markets, if a large percentage of a mortgage portfolio was originated in, say, 2022 (versus, say, the mid-2010s), then in 2025, that portfolio might look a lot more like a 2007 portfolio than anyone would like.

3. Has increased supervision and risk management reduced risks?

The reader may counter and ask, “After ‘The Crisis,’ there was a substantial increase in regulations and supervision and that led to much larger risk management functions. Maybe things are different now?” It’s possible, and while capital positions at the big banks are much higher than pre-Crisis, it is also worth noting that the increase in supervision hasn’t been uniform or consistent across banks of all sizes or across presidential administrations.

The Problem: Since the implementation of the new regulatory regime there’s no evidence that the huge investment in risk management has been worth it—largely because there hasn’t been a long and deep economic downturn.

We ask: has the generally strong credit performance across most portfolios at most institutions for the past ten to fifteen years been a result of more supervision and risk management? Or is it because, by almost all indicators, the economy has been relatively strong, the Fed has been historically accommodative, and interest rates have remained either historically or relatively low? Occam’s Razor would suggest the latter.

We aren’t saying that regulation or “enhanced supervision” is useless or should be eliminated. We are saying that no one knows if it will be effective—because it wasn’t designed to reduce already-low losses in good times.

By attributing relatively low charge-off rates to increased regulation and more risk management personnel, we might be applying a causal relationship to what may be a mere coincidence or correlation. That misattribution could increase losses in a substantial downturn.5

4. Is your portfolio more like a river or the sea?

The ocean’s salt comes from freshwater rivers, which remain fresh because, as Heraclitus noticed, they’re constantly changing—so salt doesn’t concentrate. Seawater retains salt because it has no place to go—kind of like slow-paying, marginal credits in a loan portfolio.

Let’s consider retail loans, which usually have fewer prepayment penalties than commercial ones. Better credits tend to prepay—both fully and partially—faster than marginal credits. After a period of good times, and even with constant origination criteria, portfolio composition can drift downward and begin to resemble seawater (in flavor).

Run-off portfolios tend to have even higher concentrations of the unsavory—like the Great Salt Lake or the Dead Sea—because run-off portfolios usually become run-off portfolios for credit reasons.

As mentioned above, lower-rated credits are more sensitive to exogenous (environmental or economic) factors. If portfolio segments aren’t modeled finely enough—to capture those differences in sensitivity—then forecasted losses—such as in stress test results—are likely to be understated. We’ve seen anticipated losses triple when coarse, outdated models have been replaced with more finely segmented ones.

5. Is it as calm as it seems?

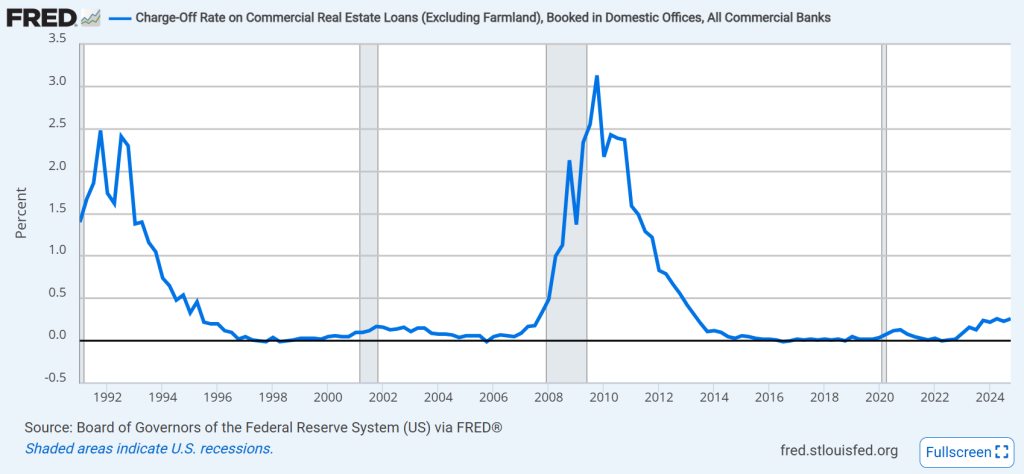

In 2025, there are clearly concerning portfolios, like CRE, with the massive volume of refinances in the next few years; credit cards, where loss rates at smaller banks—outside the top 100—are at Crisis levels; and some auto portfolios. Here, we want to address suppressed signals of trouble, and we’ll use mortgages as a prime example.

In a recent Wall Street Journal column, Allysia Finley mentioned that in the prior year, only nine—NINE—new loans backed by the FHA were foreclosed within the first 12 months of their existence.6 That doesn’t seem like a problem. That sounds like good news since FHA borrowers tend to be marginal credits.

The evidence: It’s not good news. She also notes that over 52,000 new loans—more than 7% of the total—were seriously delinquent before they were even a year old. That’s 90+ days past due in under twelve months—higher than the peak during The Crisis—and we’re not even in a downturn.7

Why so few foreclosures? Because there are programs to keep borrowers in their houses by delaying or reducing payments (and then adding the missed amounts to the borrower’s loan balance). For loans with minimum down payment of 3.5% of the price, the increase can easily put the property’s loan-to-value ratio (LTV) above 100%.

The FHA, alone, has over 500,000 mortgages in these programs, and Fannie and Freddie have similar programs. However, such programs leave the feedback loop about the health of a market dangling like an arm just after rotator cuff surgery.

They suppress negative feedback about the health of the housing market and these borrowers. These borrowers are already struggling in good times and will struggle even more in bad times, when they’re joined by other marginal borrowers who are weakened by the economy.

6. Are all innovations positive, especially for lenders?

We like to think that, despite temporary challenges, society and the economy tend to change in positive ways. But that’s not always the case. New pathologies arise and, for our purposes, affect creditworthiness, too.

Increased illicit drug use and overdose epidemics are relatively new and haven’t had positive effects for society and the economy, including on the users’ creditworthiness. Similarly, it’s hard to imagine that the legalization of online sports betting and the increased online access to risky, poorly-understood, investment vehicles will reduce consumer default rates in a downturn.

We simply note that the world is different since the last long and deep downturn, and it’s not necessarily better.8 Changes in economic policies, like new, high tariffs increase uncertainty and affect different industries and regions differently.

These innovations may increase the frequency of defaults and severity of losses beyond what we would anticipate if—as they say in the military—we’re preparing to fight the last war.

What should a banker do with the answers to these questions?

Remember that risk management involves:

- Asking what could go wrong

- Determining how much could be lost if such events occur, and

- Doing something about it—either now or contingently, when the event occurs.

We aren’t saying—explicitly or implicitly—that the economy and lenders are going to hell. We are saying that, as part of a sound risk management program, these questions are worth asking—especially for small and mid-sized lenders with regional concentrations who remain vulnerable to the broader economy.

- The deceptive nature of success

- The hidden risk in inflated asset values

- The possibly overestimated benefit of enhanced supervision

- The gradual erosion of portfolio quality through seasoning

- The illusion of calm due to delayed or suppressed signals

- The unintended negative effects of societal and technological changes

These issues can be addressed through robust stress-testing, benchmarking, and sensitivity analyses, i.e., through the application of well-informed, common-sense, quantitative methods. The true test of risk management isn’t how you perform in good times—it’s whether you’re prepared for the downward shift that inevitably occurs.

- We’re ignoring the brief recession during The Pandemic, which was both induced and mitigated by government actions. Admittedly, not all firms and individuals were made whole, but the overall economy recovered quickly. ↩

- For conciseness, we’re writing in generalities. Please indulge us. ↩

- We recognize that recent losses in some portfolios, such as credit cards at banks outside of the top 100, are at crisis levels. ↩

- Being fooled by good times can lead to cost-cutting efforts to reduce loss contingencies—such as shrinking the size of the collection department—that may decrease recoveries in a downturn. Many more examples exist. ↩

- One might argue that enhanced supervision and risk management has extended the expansionary phase of the business cycle and that everything is, indeed, different now. But, again, there are more parsimonious reasons—mentioned above—for low losses, like sustained GDP growth, low unemployment, and substantially higher asset prices. ↩

- Biden’s Mortgage ‘Relief’ Fuels Higher Housing Prices, The Wall Street Journal, February 23, 2025. ↩

- This aligns with increased risk following loosened FHA standards—now substantially more lenient than pre-2008. She cites very high Debt-to-Income (DTI) ratios as an example. ↩

- The old Problem of Induction. ↩