Insights & News

Insights on risk management, model development, loss forecasting, CECL, and stress testing from practitioners who build the models. Thought before calculation, every time.

We extend our Fort Myers Fannie mortgage loss analysis by showing how loans, ranked by expected loss rates and updated LTVs, perform if home prices decline 57%.

We then compare 2007 and 2025 portfolios to show why a crisis could re-occur.

Recent Insights

Three Components of Validation

Read more: Three Components of ValidationWe like to think of the three main components of validation like Cerebus – validation encompasses the past, present, and future. 1. Evaluation of conceptual soundness, including developmental evidence. 2. Ongoing monitoring, including process verification and benchmarking. 3. Outcome analysis, including back-testing.

Anticipated and Unanticipated Benefits of Loss-Forecasting

Read more: Anticipated and Unanticipated Benefits of Loss-ForecastingIn anticipated direct events, identification and use of risk mitigants mean better preparation to reduce losses in analyzed situations: Precautions or ex ante actions that reduce the possibility of the considered situation occurring Insurance, hedging, or other ex ante actions that reduce the magnitude of loss should the adverse event occur Contingency plan to implement ex post or actions to reduce the magnitude of…

Learning Opportunities from “A Christmas Story”

Read more: Learning Opportunities from “A Christmas Story”Learning is a benefit that is important enough to describe separately! Like much financial and credit model development, scenario analysis is research as much as development or construction. Scenario analysis leads to a better understanding of the relationships between the firm and its environment and risk factors. Note that these relationships change through time as…

SR 12-7 and the Five Principles of Stress Testing

Read more: SR 12-7 and the Five Principles of Stress TestingIf CCAR/DFAST is the extent of a firm’s stress testing, then, (a) the firm does not comply with SR 12-7, particularly Principles 1 and 2, and therefore, Principle 5; (b) there are likely deficiencies in overall risk management and data governance/systems that prevent implementation beyond CCAR; and therefore, (c ) any beneficial synergies between or among other…

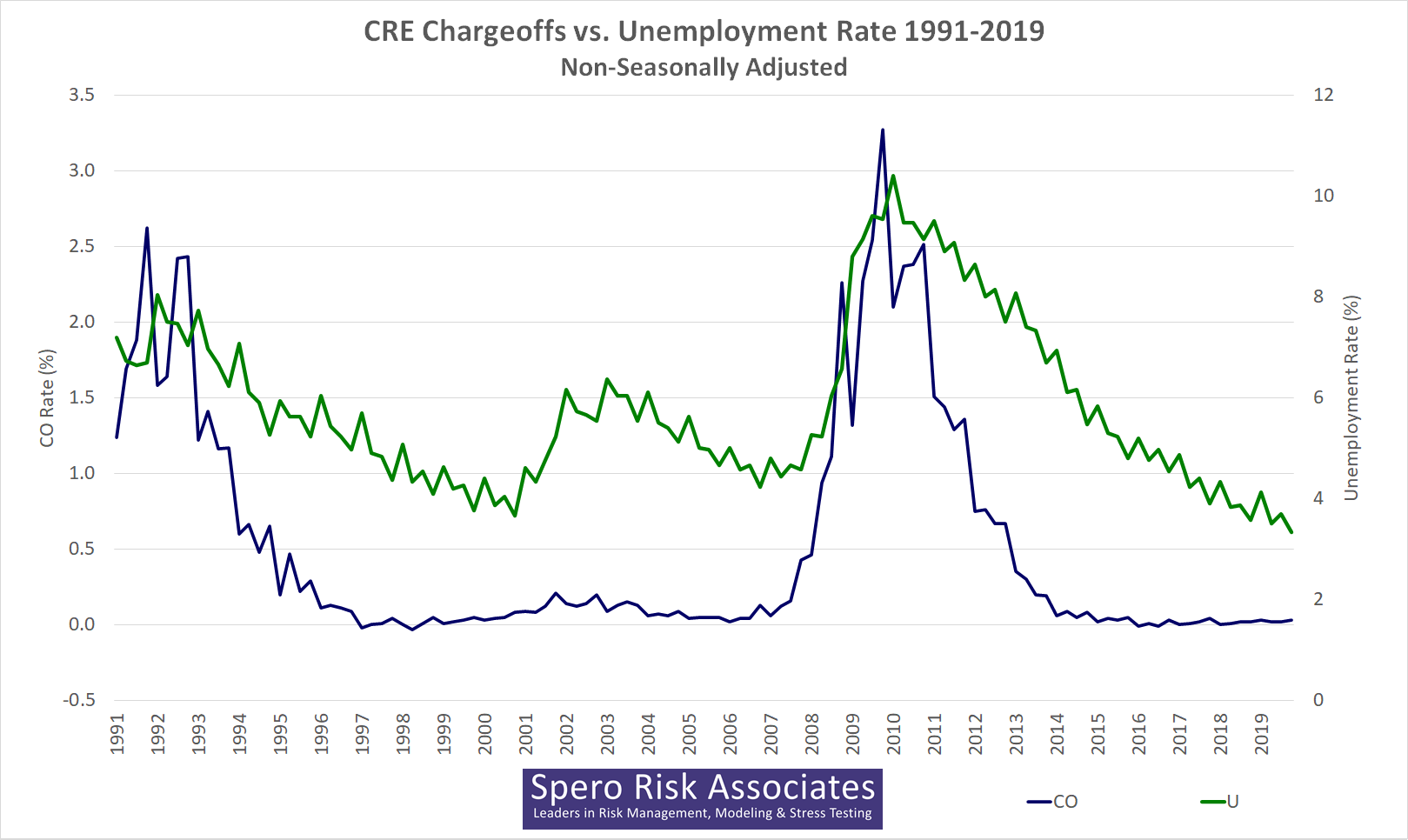

Does Unemployment Predict CRE Losses?

Read more: Does Unemployment Predict CRE Losses?The Fed’s CCAR scenario narrative always leads with unemployment; so, banks feel compelled to use it as a parameter in their loss forecasting models. The problem is that unemployment peaks tend to lag CRE (and C&I) loss peaks, which isn’t a good characteristic for an explanatory variable, especially for stress testing and risk management.

Does Unemployment Predict Commercial Loan Losses?

Read more: Does Unemployment Predict Commercial Loan Losses?The Short Answer: Historically, No, It’s the Other Way Around The Long Answer: let’s look at scatter plots and correlations and see the two large problems with using it. This is the third in a series of three posts. Two Regimes In our first post, Unemployment as a Commercial Loan Loss Predictor, we showed time-series…